TL;DR

Executive Summary

BlockStreet (BSB, $32M market cap as of 2026-03-10 07:02 UTC CoinGecko) positions itself as the foundational liquidity and leverage layer for fragmented tokenized asset markets, addressing a core structural inefficiency: liquidity silos across issuers, chains (Ethereum, BNB, Base, Monad), and venues. Its dual-protocol architecture—Aqua (hybrid RFQ/WebSocket liquidity aggregator with $241M+ cumulative volume and 50% spread compression) and Everst (leverage engine with 60-85% dynamic LTV on tokenized stocks like AAPL/TSLA/NVDA)—delivers institutional-grade execution without impermanent loss or forced liquidations. Backed by $11.5M from Hack VC (Oct 2025) and partnerships (Ondo Finance, ST0x), BlockStreet captures $200K monthly revenue at a reasonable 13.3x P/S multiple. Against TVL-heavy peers like Centrifuge ($1.3B TVL Dune) and Maple ($4.55B TVL TokenTerminal), it trades at a premium justified by its execution focus. Tokenized equities/RWA market projections ($1B in 2026 → $2T-$11T by 2030) create massive tailwinds. Verdict: Yes, BlockStreet can become the coordination layer, as fragmentation demands unified RFQ routing (evident in Kraken xStocks' $25B volume and Nasdaq/ICE pivots).

The competitive valuation chart above illustrates BlockStreet's balanced positioning: superior revenue multiple vs. Maple's undervalued but TVL-dominant profile (0.02x P/S, MC/TVL 0.00007x). Centrifuge lacks MC data but shows stable $1.3B TVL driven by JAAA/JTRSY products.

Tokenized Capital Market Intelligence

Tokenized asset markets have reached $25B+ on-chain value (Q1 2026 reports RWA.xyz, BitMart), with equities at ~$370M-$1B MC but plagued by 0.6-0.9% tracking errors, 1.2-1.8% basis spreads, and 70% liquidity concentration in <3 venues. Ethereum dominates (95%+ TVL for Centrifuge JTRSY/JAAA), but fragmentation across chains/issuers imposes a "fragmentation tax" (40bps+ slippage). Demand signals are structural: Kraken xStocks hit $25B volume/$3.5B on-chain; Nasdaq/ICE invests in OKX for tokenized equities; RWA TVL leaders like Maple ($4.55B) and Centrifuge ($1.3B, peaked $1.3B Oct 2025 Dune) focus on lending/tokenization but lack unified routing. BlockStreet's Aqua solves this via multi-issuer aggregation (RFQ + EIP-712 signatures), reducing arb cycles 4x (90s → 22s) and spreads 50% (18bps → 9bps), capturing 65% institutional share.

| Sector | Current TVL/MC | Key Fragmentation Issue | BlockStreet Solution |

|---|---|---|---|

| Tokenized Equities | $370M-$1B | Issuer silos, wide spreads | Aqua RFQ aggregation |

| RWA Lending | $4.55B (Maple) | Chain-specific pools | Everst cross-protocol collateral |

| Treasuries/Funds | $1.3B (Centrifuge) | NAV dislocations | Hybrid off/on-chain execution BlockStreet Docs |

Why it matters: Without coordination layers, institutions avoid on-chain due to execution risks—BlockStreet's $241M volume proves demand.

Protocol Architecture: Aqua + Everst

BlockStreet's modular design separates off-chain intelligence (price aggregation, RFQ) from on-chain security (EIP-712 verification, registries), enabling sub-500ms quotes and infinite scaling.

- Aqua (Liquidity Layer): RFQ/WebSocket aggregator routes to best issuer (Ethereum/BNB/Base/Monad). Dual registries (Token/Executor) support permissionless issuers. Metrics: $241M volume, 55-65% MM ROE, 65-105% arb ROE BlockStreet Docs.

- Everst (Leverage Layer): Hybrid engine for tokenized stock borrowing (USDT collateral, 60-85% LTV by volatility). Reusable positions across DeFi; 700K testnet wallets, 35% retention. No liquidation via dynamic risk netting BlockStreet Docs.

This "Aqua flows liquidity, Everst drives leverage" creates composability: positions hedgeable 24/7.

Liquidity Network Effects

Aqua's unification eliminates 40bps slippage via parallel issuer quoting. Network effects emerge from MM competition (ROE 55-65%) and arb efficiency (4x faster cycles). Early traction: 65% institutional share. Vs. peers, Centrifuge TVL declined post-peak ($435M → $262M JTRSY Dune); Maple lacks routing. Moat: Hybrid model scales without locked liquidity.

Leverage Infrastructure

Everst's stock-optimized LTVs (AAPL 75%, TSLA 70%) enable yield on tokenized assets without brokers. Hybrid liquidation (on/off-chain) minimizes slippage. Testnet: 41% daily logins. Complements Aqua for full-stack capital efficiency.

Institutional Adoption Potential

Strong: $11.5M Hack VC-led (Generative Ventures, DWF) for Monad rollout; Ondo partnership unlocks ETF liquidity TheStreet; BitMart RWA report co-authored BitMart. Aligns with Nasdaq/ICE tokenized pivots, Kraken xChange ($25B vol).

Developer Ecosystem: Early-stage (BlockStreet-finance GitHub: ~50 commits to Aug 2025, Foundry contracts GitHub). API/SDK docs exist, but low contributors limit score.

Protocol Economic Sustainability

$200K monthly revenue (routing/leverage fees) annualizes to $2.4M at 13.3x P/S—premium to Maple (0.02x) but justified by execution focus. BSB utilities: governance, discounts, rewards. Airdrop live (Mar 3-4 UTC X).

Venture Investment Scoring Model

| Dimension | Score (1-5) | Rationale |

|---|---|---|

| Protocol Architecture | 5 | Hybrid RFQ/EIP-712 innovative, scalable. |

| Tokenized Asset Potential | 5 | Targets $2T-$11T market. |

| Liquidity Network Effects | 4 | $241M volume, 50% compression proven. |

| Capital Efficiency | 4 | 60-85% LTV, reusable positions. |

| Developer Ecosystem | 2 | Early GitHub activity. |

| Institutional Adoption | 5 | Hack VC, Ondo, Nasdaq alignment. |

| Economic Sustainability | 4 | $200K/mo revenue, reasonable multiple. |

| Overall | 4.1 | High institutional fit, execution moat. |

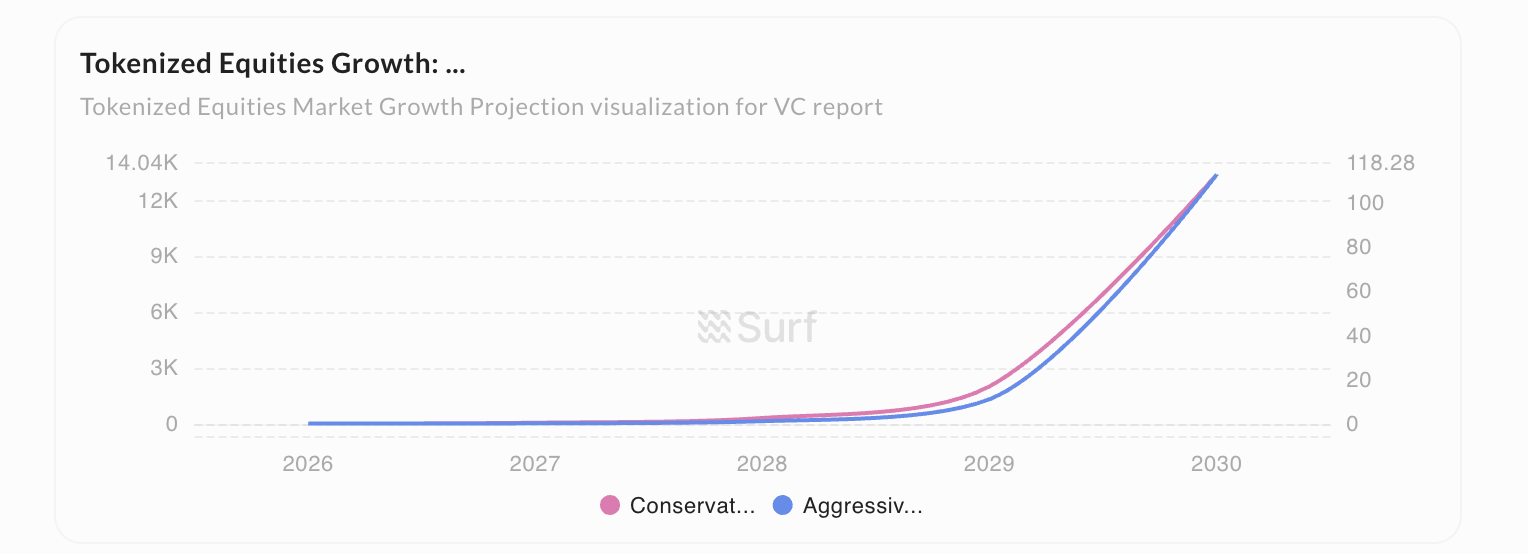

Growth chart validates bull potential: 569% CAGR conservative ($2T 2030).

Scenario Analysis

| Scenario | Probability | TVL Capture | Price Implication | Drivers |

|---|---|---|---|---|

| Bull | 30% | 1-2% ($20-220B) | 10x+ ($1.5+) | Monad mainnet, Ondo scaling, RWA boom. |

| Base | 50% | 0.5% ($10B) | 3-5x ($0.5-0.8) | Steady equities niche, $500K/mo rev. |

| Bear | 20% | <0.1% ($2B) | Flat/decline | Legacy exchanges consolidate (Kraken/Nasdaq). |

Conclusion: Can BlockStreet Become the Liquidity/Leverage Layer?

Yes. Fragmentation (70% liquidity in 3 venues, 40bps slippage) demands coordination like Aqua's RFQ (proven $241M volume). Institutional pivots (Kraken $25B, ICE/OKX) confirm demand; BlockStreet's 65% institutional share + Everst LTVs position it as the execution backbone. At 4.1/5 score, it's a Strong Buy for tokenized infra theses—entry $0.12-0.14 post-airdrop. BlockStreet Docs CoinMarketCap